Introduction

Mustang sold 635 in June and this is down 42.2% on the year to date numbers for last year, no doubt caused by the run out of stock before the new (and much improved) model arrives later this year.

The Commodore looks to be nearing the end of run out but sales of the new model improved to 1,159 units (895 less than in 2017) while the Aurion sold 5 as it also fades away.

For the year to date the total passenger market is up by 0.7% or 3,995 units and although June sales were better than May, the overall rate of growth has slowed on a year to date basis.

The top sellers for this month see some changes to the bottom half of the top 10 amongst passenger vehicles. The Toyota Corolla (3,780) retained the overall lead ahead of the Hyundai i30 (3,547) which retained 2<sup>nd</sup> place with the Mazda 3 (3,327) in 3<sup>rd</sup>, all unchanged. The Mazda CX-5 (3,136) remained in 4<sup>th</sup>; Toyota RAV 4 (2,690) remained 5<sup>th</sup>; Kia Cerato (2,485) gained two places to 6<sup>th</sup>; VW Golf (2,317) remained in 7<sup>th</sup>; the Honda CR-V (2,232) gained six places to 8<sup>th</sup>; Nissan Qashquai (2,198) gained fourteen places to 9<sup>th</sup> and the Nissan XTrail (2,151) gained one spots to round out the Top Ten.

Worth noting: the Nissan Qashqai gained fourteen places and the Honda HR-V gained eleven while the Toyotas Prado lost eight places and the Toyota Camry lost ten places.

If we were to include the 4x4 Utes in the listing, then the Ford Ranger is in 1<sup>st</sup> place, Toyota Hilux comes in at 2<sup>nd</sup> overall; the Mitsubishi Triton is 4<sup>th</sup> and the Holden Colorado takes 12<sup>th</sup> place. No Ford models made it inside the Top 25 and sixteen of the Top 25 come from the one of the SUV categories.

The Large segment lost market share to 1.18% of the market in June and it has dropped 46.9% (6,258 units) in volume compared to 2017.

The top selling passenger vehicle sales are shown below:

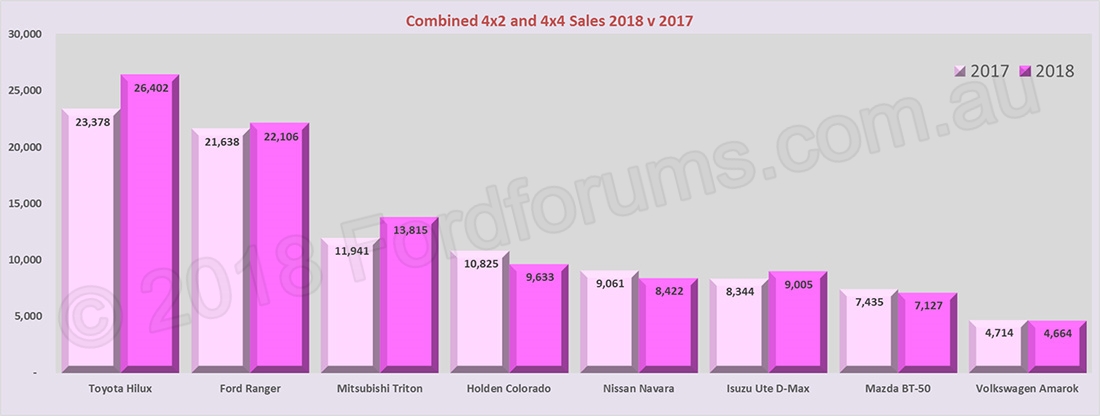

.. and the same chart with the 4x4 Utes included.:

The chart below looks at the large segment slide in comparison to the Light (Fiesta), Small (Focus) and Medium (Mondeo) segments during the last ten years from a dominant position to almost at the bottom.

Ute 4x2

The Falcon Ute is gone now and wont be included in future charts except where historically appropriate. Ranger sales were steady with 532 sold during the month, 70 less than the same time last year.

The Ford Ranger (down 6.1%) dropped to 3<sup>rd</sup> place this month behind the Toyota Hilux (1,755) and Isuzu Ute D-Max (605) but in front of the Mazda BT-50 (452) and Nissan Navara (348), all unchanged except the Isuzu which gained a place.

For 2018 YTD the segment is now down 4.68% (991 units) and it held a slightly smaller 3.53% of the market.

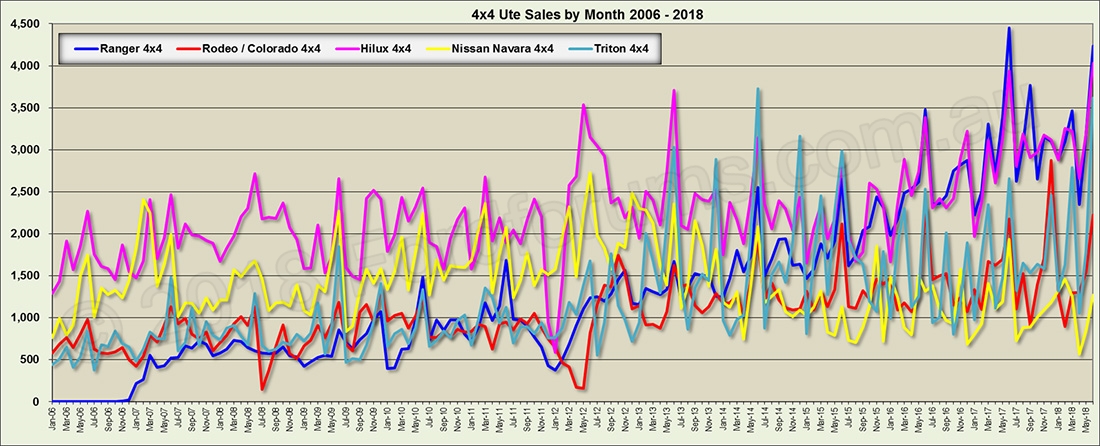

4x4 Utes

The 4x4 Utes held an improved 17.09% of the total market during the month and their segment sales are now only up 7.09% (5,893) for the year. Most of the major contenders have made gains compared to the same period last year Triton (+18.1%), Hilux (+12.2%) and Ranger (+3.5%) with only the Holden Colorado (-11.2%) and Nissan Navara (-8.8%) taking a hit.

The Ford Ranger (4,236) regained the segment lead from the Toyota Hilux (4,032) while the Mitsubishi Triton (3,614) remained in 3<sup>rd</sup>, the Holden Colorado (2,221) remained in 4<sup>th</sup> and the Isuzu Ute D-Max (1,616) gained a place to 5<sup>th</sup>.

Given the movement in the 4x4 and 4x2 Ute segments, we are going to include the previous quarterly analysis of how they are performing year against year in this report and report on it monthly instead. The only entrants included are those with both a 4x2 and 4x4 entrant so that does leave some out but nothing with any significant volume.

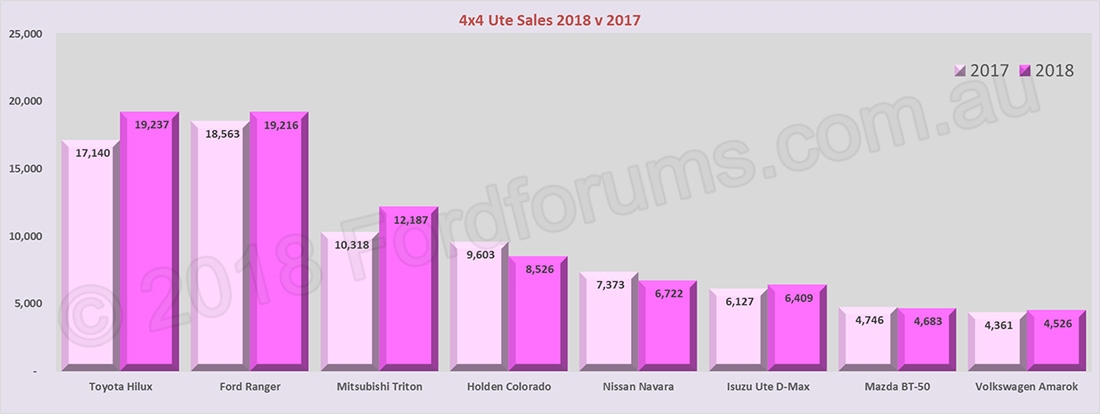

And a closer look at the 4x4 Utes only

The final chart depicts the combined Holden and Ford sales for 4x2 Utes as a percentage share. This looks at the period from January 2012 when they both had two entries in the market place and as the Ranger continues, this chart will remain.

Prestige Segment

The Caprice, also in stock run-out mode managed no sales and the luxury segment is down 10.78% overall. Chryslers 300/C managed 14 sold in June to be up 4.3% on this time last year. With no Ford entrant in the category we no longer graph this category.

Fiesta / Light Segment

The Hyundai Accent (1,522) retained the segment lead with the Mazda 2 (1,149) in 2<sup>nd</sup> and the Toyota Yaris (1,056) in 3<sup>rd</sup>, all unchanged.

The rest of the top group consists of:

Suzuki Swift (1,004) steady in 4<sup>th</sup>;

Honda Jazz (852) steady in 5<sup>th</sup>;<sup>

</sup>Kia Rio (846) steady in 6<sup>th</sup>;

Holden Barina (425) up two places in 7<sup>th</sup>; and the

Ford Fiesta (23) down one place in 14<sup>th</sup> and only outselling the MG3.

This segment held a lower 6.55% of the total market in June and is down compared to 2017 by 4.45% (1,898 units). Not surprisingly, its downward results for about half the contenders in the segment with the Toyota Yaris down 20.1%, Mazda 2 down 11.0%, Fiesta down 52.3% and VW Polo down 29.3%. Kia Rio +10.9%, Holden Barina +19.5% and Suzuki Swift +76.3% are the biggest winners.

Please note we have shortened the time scale on some of the segment graphs as they were getting too difficult to read over the longer term.

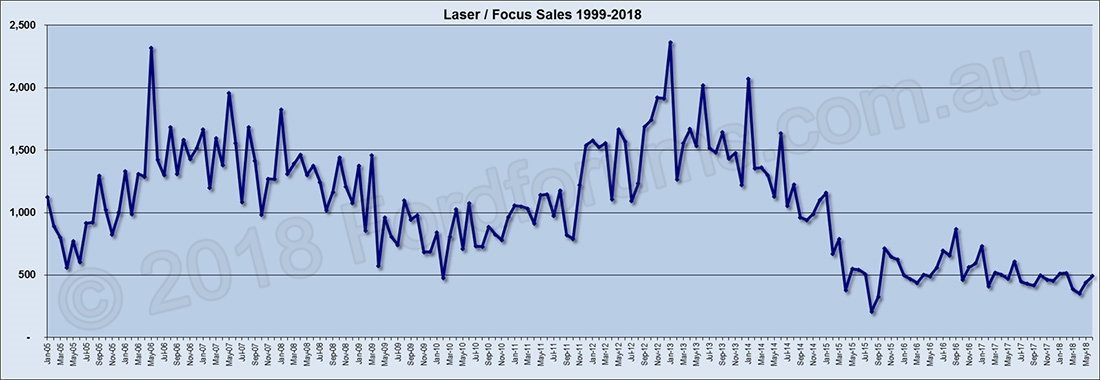

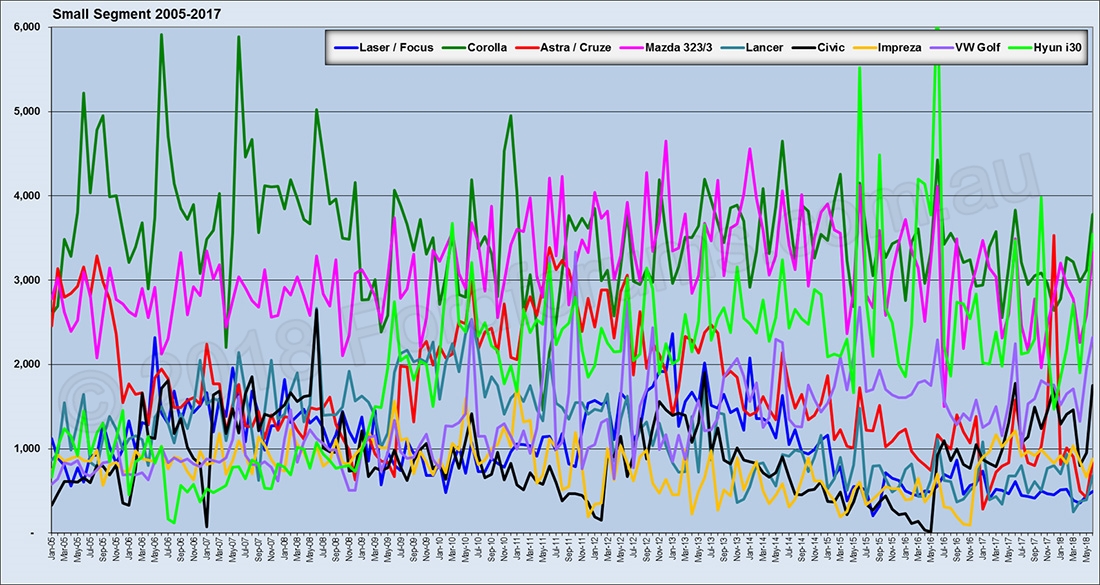

Focus / Small Segment

The month saw Focus back down three places to 11<sup>th</sup> place with 491 sold, a pleasing result in what has been a torrid time. The segment lead was retained by the Toyota Corolla (3,780) ahead of the Hyundai i30 (3,547) in 2<sup>nd</sup> with the Mazda 3 (3,327) still in 3<sup>rd</sup>.

The remainder of the Top ten are:

Kia Cerato (2,485) up a place in 4<sup>th</sup>;

VW Golf (2,317) down a place to 5<sup>th</sup>;

Honda Civic (1,750) steady in 6<sup>th</sup>;<sup>

</sup>Subaru Impreza (877) steady in 7<sup>th</sup>;

Holden Astra (851) up a place in 8<sup>th</sup>;

Mitsubishi Lancer (673) up a place in 9<sup>th</sup>; and

Hyundai Elantra (498) up a place to 10<sup>th</sup>.

For the year to date, Corolla is down 1.6%, the Mazda 3 is down 5.3%, the Focus down by 16.8% andthe Subaru Impreza down 18.9%. On the winning side, Honda Civic is up 16.9%; VW Golf up 16.5% and Hyundai i30 up 3.0%.

The segment held a slightly bigger market share of 18.18% in June and it is down overall by 3.8% (4,263 units) compared to 2017.

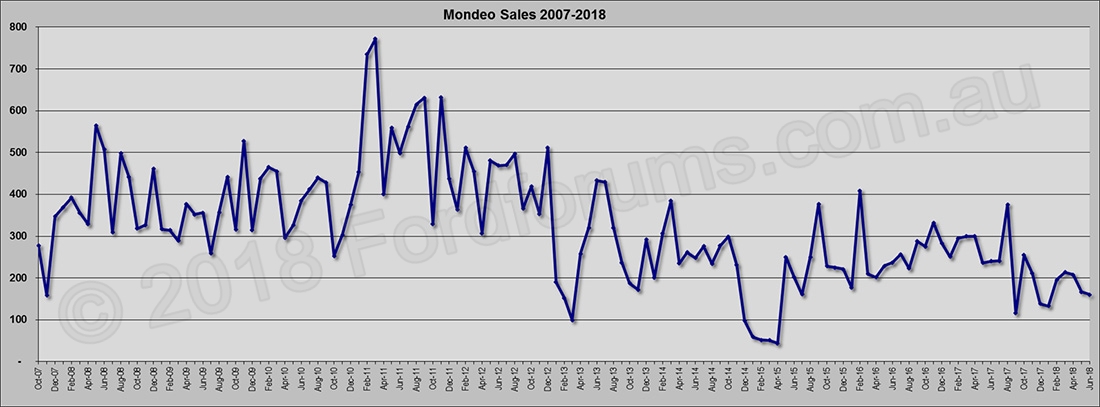

Mondeo / Medium Segment

In June, 160 Ford Mondeos were sold and it lost another place to be in 5<sup>th</sup> place. The segment lead was retained by the Toyota Camry which sold 1,380 with the Mazda 6 (405) still in 2<sup>nd</sup> and the Volkswagen Passat (214) up a place in 3<sup>rd </sup>with the Skoda Ocatvia (210) down one place to 4<sup>th</sup> and the Subaru Liberty (148) steady in 6<sup>th</sup>. If they were counted on size and not price the Mercedes C Class (484), CLA-Class (420) and BMW 3-Series (351) would have been in the top five.

Percentage wise, the Skoda Octavia (+16.0%) is the only winner compared to 2017 with the Subaru Liberty (-26.5%), Mondeo (-33.5%) and Honda Accord (-52.7%) the biggest losers and even the perennial Camry has dropped 35.9%.

The segment held a smaller 2.31% of the market in June and has lost volume by 29.48% compared with 2017 a drop of 6,204 sales and it really is rapidly becoming as irrelevant a segment to contend in as the large segment has been for some years.

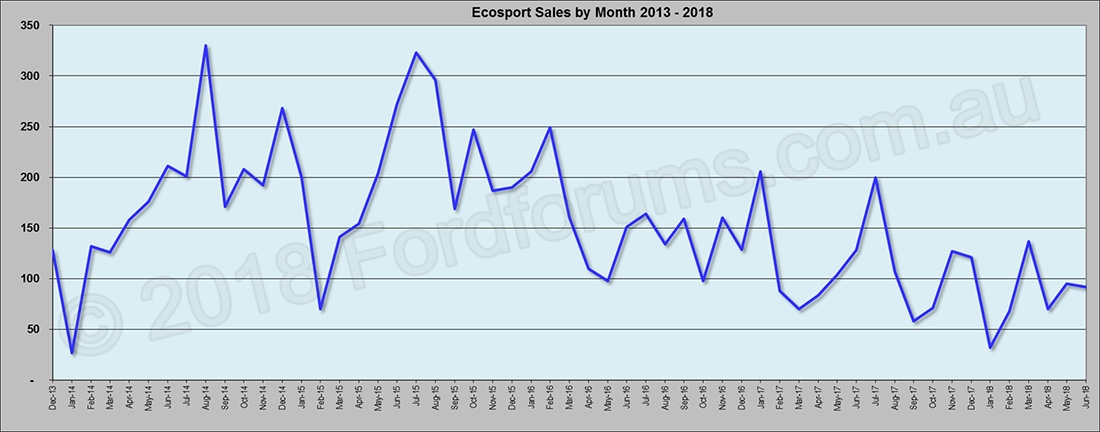

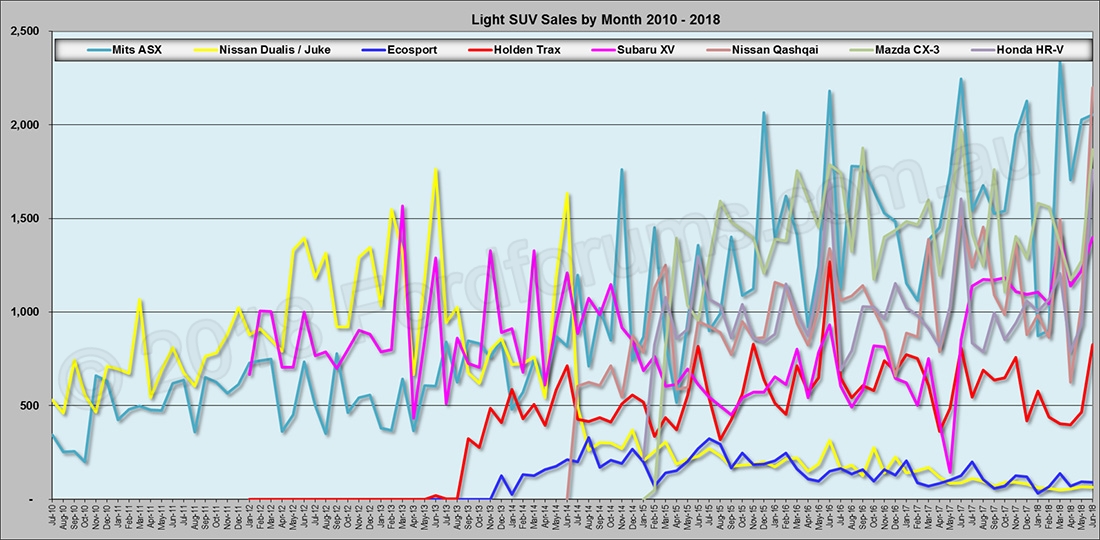

Ecosport / Light SUV Segment

During June, the Ford Ecosport sold a mere 92 units but it remained in 14<sup>th</sup> place with the rest of the order being:

Nissan Qashqai (2,198) up four places to take the segment lead;

Mitsubishi ASX (2,053) down a place in 2<sup>nd</sup>;

Mazda CX-3 (1,869) down a place in 3<sup>rd</sup>;

Honda HR-V (1,760) up two places in 4<sup>th</sup>;

Subaru XV (1,399) down a place to 5<sup>th</sup>;

Hyundai Kona (1,317) down a place to 6<sup>th</sup>;

Toyota CH-R (915) steady in 7<sup>th</sup>.

Please note that we have realigned our stats with the VFACTs categories now that there is a Ford entrant in this segment.

Mostly losers in this segment, the Nissan Juke is down 52.4%, Holden Trax down 18.1% and the Ecosport down by 27.4%. On the other side, Subaru XV is up 123.1% and the Mitsubishi ASX up 9.5%.

The segment held a larger 11.51% of the market in June and it is up 30.76% (15,006) compared to 2017.

Escape / Compact SUV Segment

During June, the Escape sold 482 units and remained in 11<sup>th</sup> place with the top positions held by:

Mazda CX-5 (3,136) retaining the segment lead;

Toyota RAV-4 (2,690) steady in 2<sup>nd</sup>;

Honda CR-V (2,232) up two places in 3<sup>rd</sup>;

Nissan X-Trail (2,151) steady in 4<sup>th</sup>;

Hyundai Tucson (2,000) down two places in 5<sup>th</sup>;

Mitsubishi Outlander (1,881) steady in 6<sup>th</sup>; and

Kia Sportage (1,499) steady in 7<sup>th</sup>.

Most contenders are now up in volume for the YTD with only the Ford Escape down 4.9%, Hyundai Tuscon down 19.9% and Subaru Forester down 24.6%. Honda CR-V is up 201.0%, Toyota RAV4 up 8.9% and VW Tiguan up 7.6%.

The segment held a larger 16.2% of the market in June and it is up 10.0% (8,293 units) compared to 2017.

Territory / Medium SUV Segment

The segment lead was regained by the Toyota Kluger (1,757) ahead of the Toyotas Prado (1,688) which dropped to 2<sup>nd</sup> with the Subaru Outback (1,152) steady in 3<sup>rd</sup>. The rest of the Top 10:

Isuzu Ute MU-X (1,056) holding on to 4<sup>th</sup>;

Mazda CX-9 (941) up two places to 5<sup>th</sup>;

Hyundai Santa Fe (847) steady in 6<sup>th</sup>;

Mitsubishi Pajero Sport (645) up four places to 7<sup>th</sup>;

Holden Captiva (560) up two places to 8<sup>th</sup>;

Ford Everest (514) steady in 9<sup>th</sup>; and

Kia Sorento (468) down four places in 10<sup>th</sup>.

Prado (+7.1%), Kluger (+26.0%) and Everest (+31.1%) are all better than last year with only the Captiva (-41.8%) and Pajero + Sport (-15.5%) showing any substantial drop. Despite the mixed individual performances, the segment held a smaller 9.92% of the market in June and has dropped volume by 4.73% for the year to date a decrease of 2,899 sales.

The second chart depicts sales for the Territory and Everest over the entire production life.

Market Share Analysis

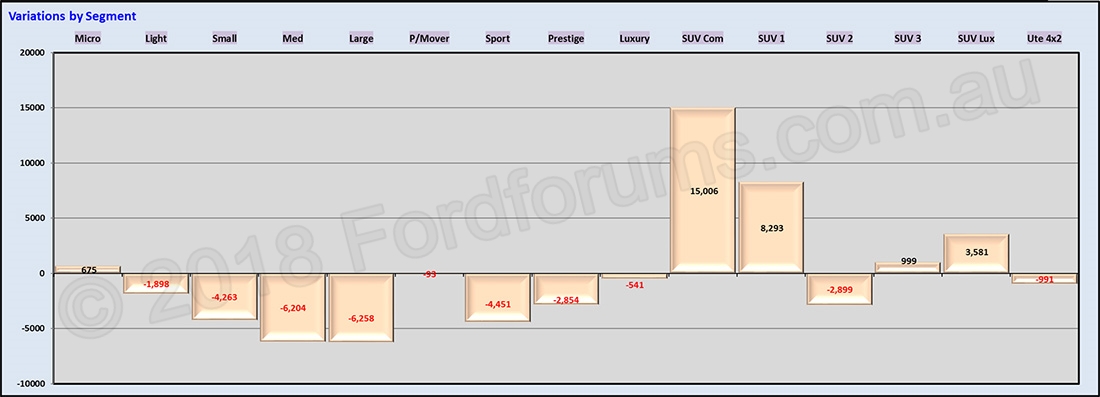

For an easy look at the share held by each market segment, we have included a set of graphs that display this for quick reference the first looks at the percentage market share for the current month while the second compares the percentage numbers for the current month for the last three years where is easy to see quickly which segments have gained and which have lost. We have also added a look at the segment movements in raw numbers terms for the month YTD. This shows the actual unit numbers that have been gained or lost within each segment for the year to date.

Total Market

Toyota retained the passenger market leadership in June with 22,914 passenger segment sales giving them a comfortable lead over Mazda (12,469); Hyundai (10,436) in 3<sup>rd</sup>; Mitsubishi (10,232) in 4<sup>th</sup>; Ford (7,418) steady in 5<sup>th</sup>; Holden (7,385) up two places to 6<sup>th</sup>; Kia (7,067) down a place in 7<sup>th</sup>; Nissan (6,604) up a place in 8<sup>th</sup> and VW (6,334) down one place to 9<sup>th</sup>.

In percentage terms Ford is down 10.9% on 2017, Mazda down 3.5% and Holden are down 22.6%. On the positive side, Mitsubishi is up 10.6%, Kia is up 9.1% and Toyota is up 2.4%.

The chart below looks at the same data but over a shorter time frame so that movements are a little easier to detect.

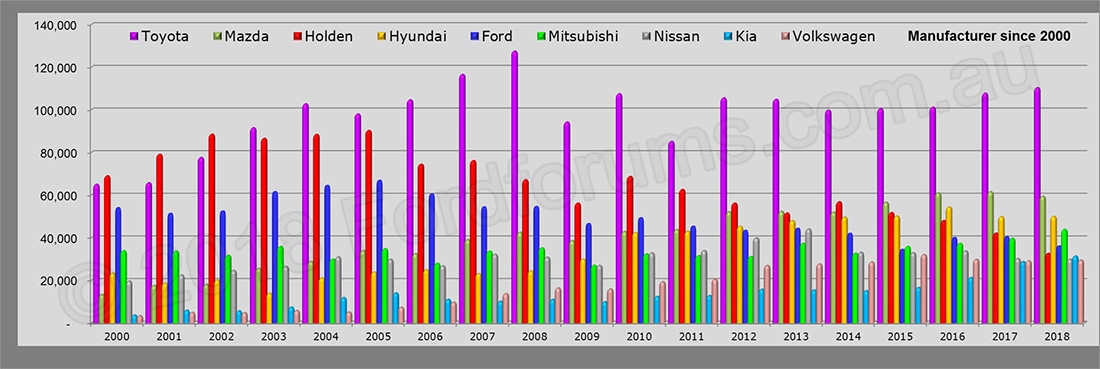

We have been taking a look at the 15+-year history of the four manufacturers (Ford, Holden, Mazda and Toyota) from 2000 to the current time. These figures are based on year to date sales and as well as making the recent gain in the overall market apparent they also clearly depict how Toyota has pulled away from everyone since 2003; Mazdas gain (and overtaking) of Ford in the 3<sup>rd</sup> to 5<sup>th</sup> place battle and the increasing penetration of both Nissan and Hyundai.

The next set of charts look at the trends within each segment and draws some comparisons between various battles within them.

Please note that these graphs are based on the percentage share of the total market and as the market has been growing each year for the last decade or so (with the exception of 2009) the actual gains or losses are significantly greater than the gradual changes shown in the graph.

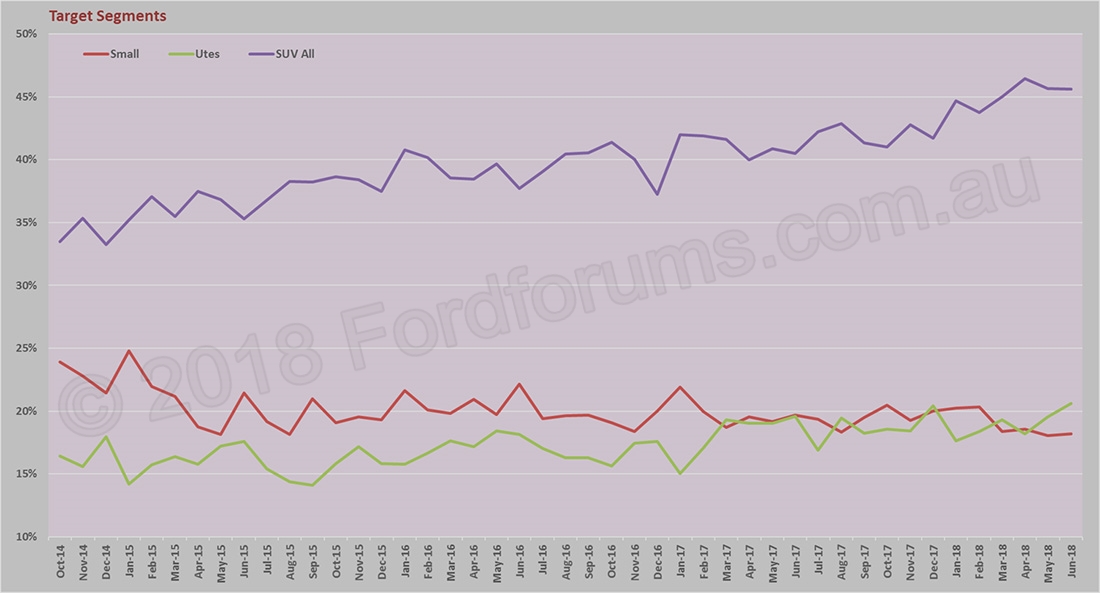

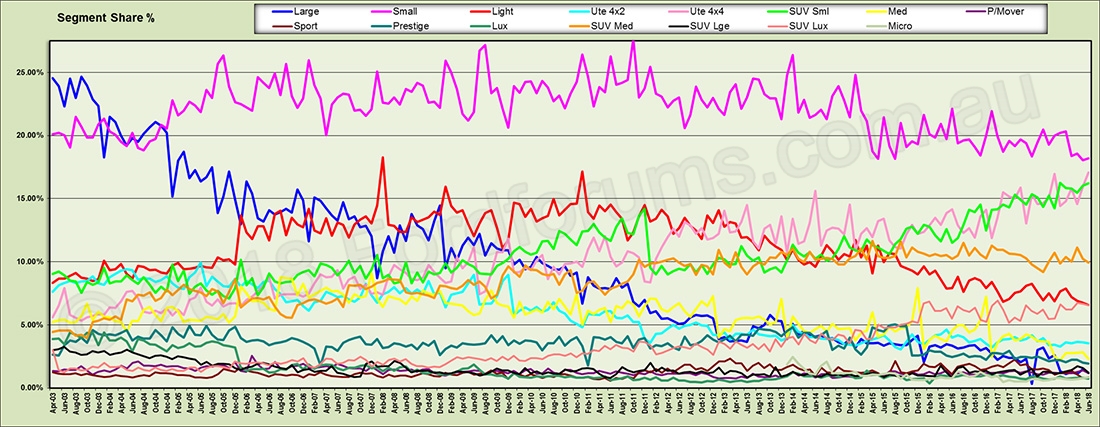

First up is a look at the four passenger segments where we can clearly see the continued slide in the large car segment, the strength of the dominant small segment and the rise in the light segment.

.. and a more targeted look at three critical segments over a shorter time frame:

Second is the percentage share held by each segment during the last five years worth noting is the impact of the SUV realignment and the continued, if somewhat inconsistent, strength of the small segment.

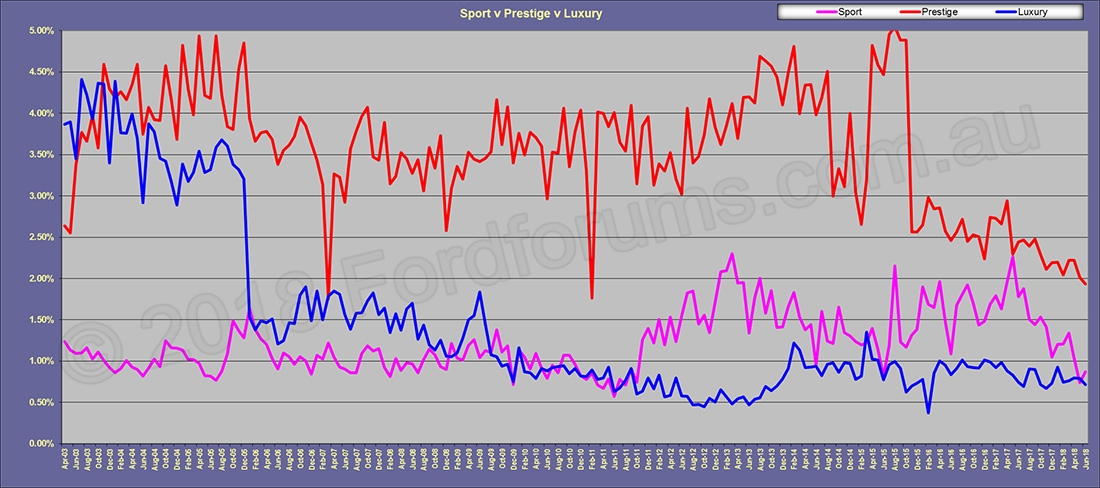

Third is a closer look at the sport, prestige and luxury segments over the same time frame. While some of the vehicles that get placed in these categories defy logic they are the segments that are a good indicator of the general economic performance in Australia and they had all trended slightly downward but appear to have rallied so far this year.

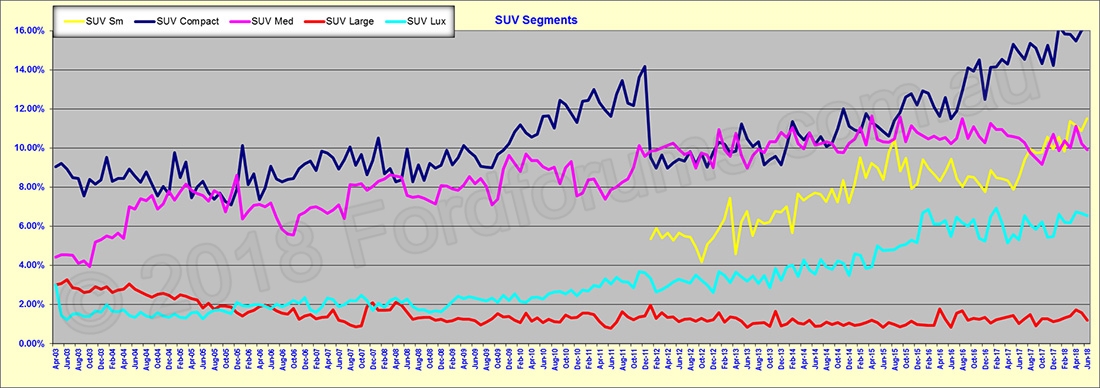

Fourth is a look at the SUV segments. These segments had been growing quite rapidly and most of that growth had been in the compact and medium sized vehicles but after the realignment this year the medium segment now has the upper hand over the compact segment most of the time although it is inconsistent. We have included the new segment for completeness.

To see who the winners and the losers are so far this year here is a comparison of the various manufacturers on a YTD basis when compared to last year. For the purpose of the exercise we have obviously picked the (modern) big four; Toyota, Holden, Mazda and Ford but also added a couple of others that have been big movers in recent times by way of comparison. The first chart looks at the raw numbers while the second looks at the percentage variation. Drilling down on the winners and losers a bit more shows some interesting changes amongst both manufacturers and individual models.

The biggest overall improver is Honda, gaining 7,470 sales which represent a 34.2% improvement on 2017. Toyota gained 2,828 sales but that is only a 2.8% increase. Others in the better than 10% improvement club include Isuzu Ute (+18.4%); Mitsubishi (+10.6%), and Ferrari (+19.8%) although the latter is based on very small volume.

The biggest overall loser is Holden, down 22.6% and 9,499 sales although Jaguar dropped 14.7% and Infiniti lost 30.1% albeit also on very low volume.

In terms of individual models, the Honda CR-V (6,025) has gained the most sales ahead of the Subaru XV (4,045), Toyota Hilux 4x4 (2,097), Toyota CH-R (2,382) and Suzuki Swift (1,889).

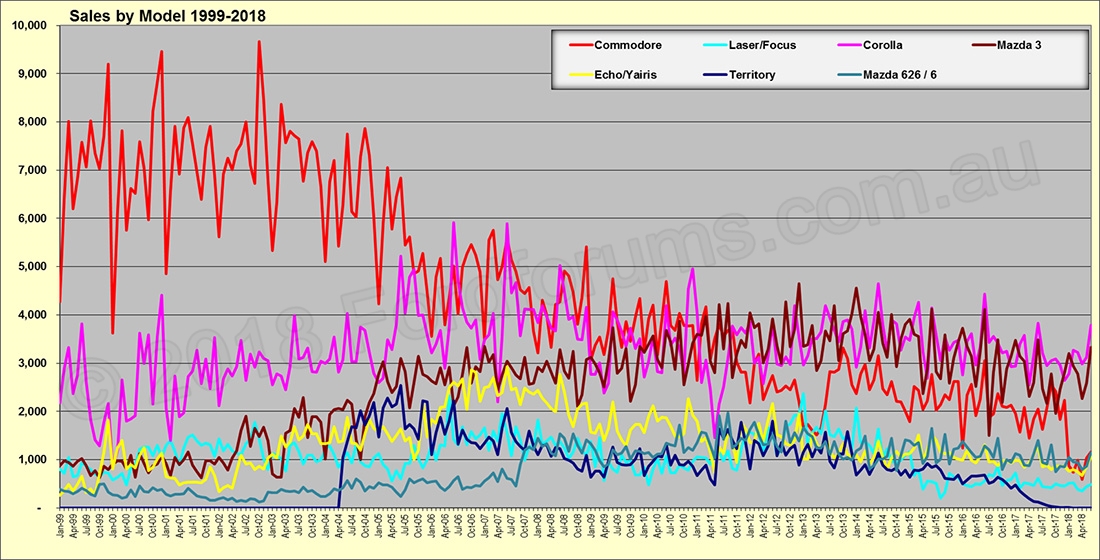

Next up is a look at some individual models naturally all of the current Ford range with any real volume has been included but also the segment leaders and the red corner competition along with anything else that seemed of interest.

.. and a (newer) comparison of all the non-Falcon based Ford models. Please note that the Mustang is now included.

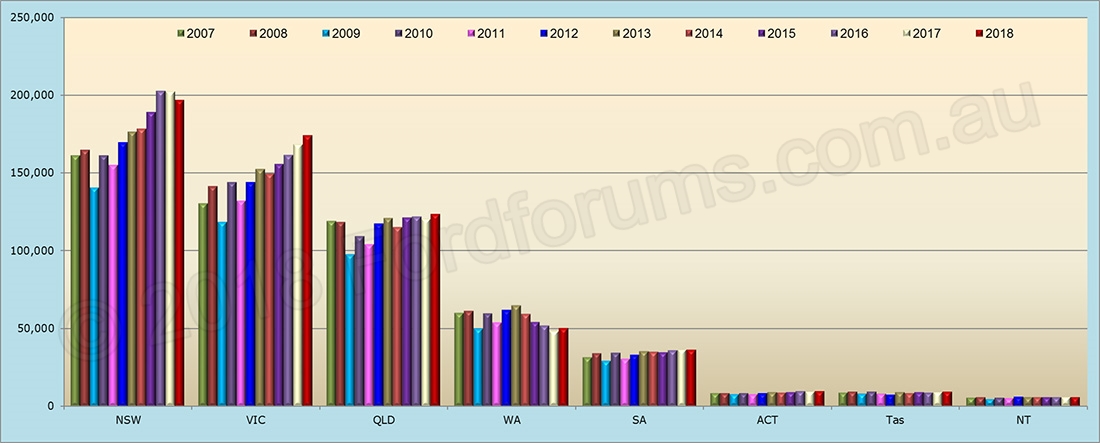

State of Origin

We also take a quick look at the sales by State. The data is for the year to date and looks at the years from 2007 to 2018. All of the States gained volume for the year to date except NSW which is down 2.8% and the NT down 0.4%. West Australia and Tasmania the biggest winners with 3.8% and 3.9% growth, respectively. All except WA (-21.9%), Northern Territory (-1.0%) and Tasmania (-0.4%) have improved compared to ten years ago with Victoria (+18.8%) the biggest improver over that period.

The first chart looks at the raw sales numbers over the period while the second compares the percentage change between 2017 and 2018.

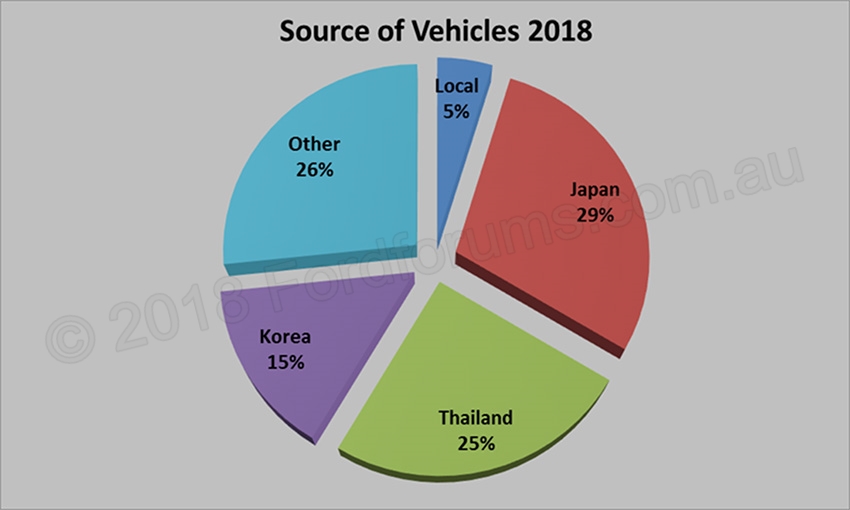

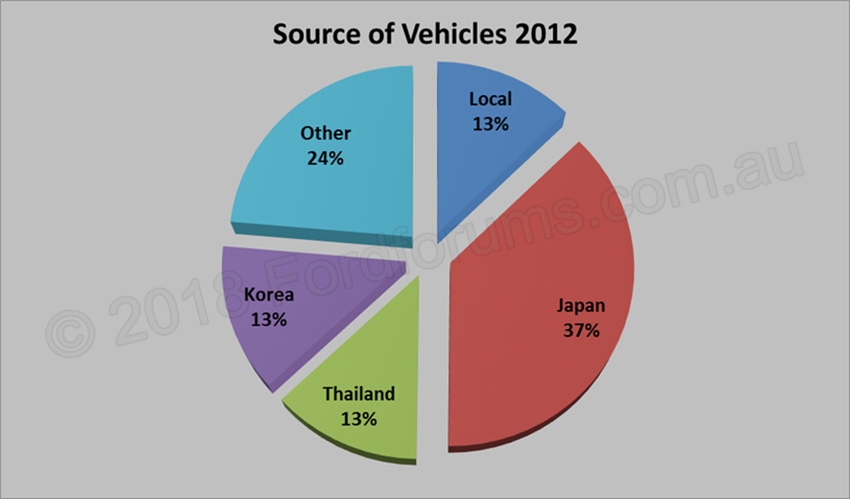

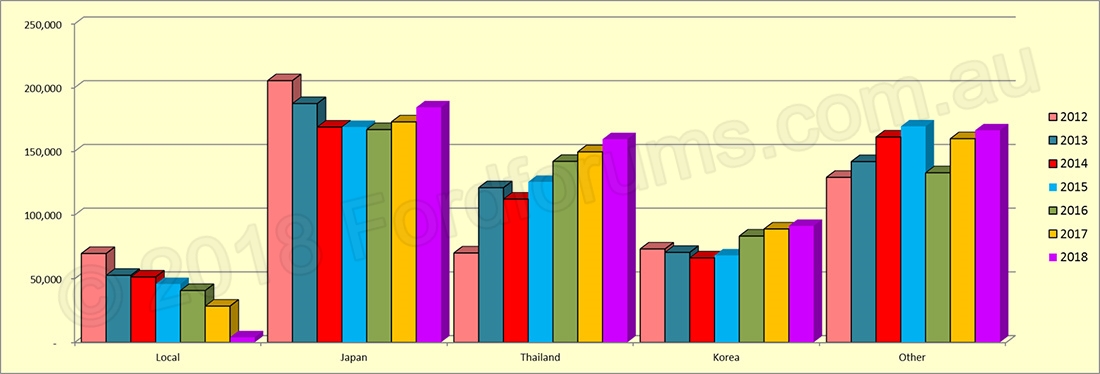

Country of Origin

Finally, a little look at the origin of our vehicles - not really a concern now that we know the future of our automotive industry but it does at least show where some of the production off shore originates.

The pie chart shows the major origins for vehicles sold in the Australian market on a YTD basis (along with a comparison from 2012) while the second chart compares those figures to the previous years and the final chart shows a YTD total (by year) for all imports compared to locally produced.

Ford Australia Sales Stats June (06) 2018

Ford Australia Sales Stats June (06) 2018

Drilling down on the winners and losers a bit more shows some interesting changes amongst both manufacturers and individual models.

Drilling down on the winners and losers a bit more shows some interesting changes amongst both manufacturers and individual models.

Be The First